In the face of higher costs, more Canadians are changing their grocery shopping habits, hunting for bargains and switching to lower-cost brands — yet many are leaving money on the table when it comes to their single largest transaction.

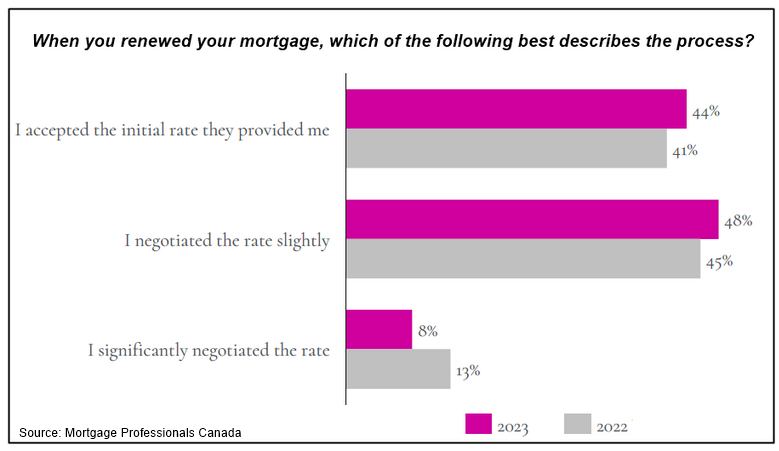

According to a recent survey conducted by Mortgage Professionals Canada, homeowners are doing less haggling at renewal, despite most facing higher interest rates.

The study found that 41% of borrowers accepted the initial rate offered by their lender, up from 37% two years ago. Furthermore, just 8% say they “significantly” negotiated their rate at renewal, down by half since 2021, when 16% haggled aggressively.

“You’d assume that people would be shopping more than ever in the face of ‘renewal shock,’” says Robert Jennings of St. John’s Newfoundland-based East Coast Mortgage Broker. “In the second half of 2019, mortgage rates were well under 3%, so the mortgages that come up for renewal on a go-forward basis, rates are close to double.”

Canadians are leaving money on the table

Jennings says the MPC data is frustrating to see, given how much Canadians could be saving by working with a broker or shopping around for a better deal. He speculates that many are unaware that rates can be negotiated, and suggests that banks are being more aggressive and reaching out to clients earlier to lock them in at above market rates.

“Some bankers would even go as far as saying, ‘hey, here’s your renewal offer, if you find a better rate, tell me and I’ll try and match it,’” Jennings says. “How unethical is that? You’re telling somebody, ‘Hey, you probably can’t afford this, but we’re going to give it to you anyway, and we’re not going to give you our best rate unless you can go find a better rate.’”

Jennings adds that he finds it ironic how Canadians will spend hours on the phone haggling with their telecommunications provider to save a few bucks each month on their phone, internet and cable bills, but don’t know they should be doing the same with their mortgage. Like those telecom companies, he says most lenders save their best deals for new customers, meaning that there’s usually a better deal to be had elsewhere.

“If you know that going into your renewal, you should have the mindset of ‘I’m going to actually change my mortgage,’ as opposed to, ‘I want to stay with my bank,’” he says. “You should be offended by the interest rates that they offer.”

How rate shopping could save borrowers thousands of dollars

The potential savings from switching can also be quite significant. A borrower with a $450,000 mortgage on a 25-year fixed term that’s up for renewal after their first five, for example, can currently find interest rates ranging from 4.79% to 5.5%, according to Nolan Smith of Nanaimo-B.C.-based TMG Oceanvale Mortgage & Finance.

“We’re talking $170 less per month, which is your gas bill or maybe a chunk of your groceries, and that’s just picking a different lane,” he says. “The other thing is the balance remaining at the end of your new five-year term is about $5,000 lower, so you’re paying $5,000 more off your principal while saving $170 per month, which is about $10,000 over five years, which works out to $15,000 [in total].”

Fear and uncertainty could be to blame

Smith says Canadians wouldn’t knowingly accept a higher payment if they knew a better deal was a phone call away and suggests that many are acting out of fear. He explains that there has been a lot of negative news about mortgage renewal rates as of late, and that could be spooking borrowers into taking the first offer.

“When people get scared about what’s going on, they kind of glob onto what they know,” he says. “That could be a reason why people are just listening to what their institution is saying.”

According to a separate Leger survey, six in 10 Canadian mortgage holders — and 68% of those between 18 and 34 — say they are financially stressed. With many facing more difficult economic circumstances Ron Butler of Toronto-based Butler Mortgages says perhaps they’re afraid to negotiate because they’re concerned about qualifying.

“It’s very unlikely that isn’t a contributing factor,” he says. “But there is a difference between not caring and being scared that someone will say ‘no’ — I don’t believe people don’t care.”

In fact, the survey results — which suggests that Canadians are doing less haggling in a higher interest rate environment — is so counterintuitive that Butler finds it difficult to believe.

“I hardly believe that anybody today just cheerfully signs the first offer their lender gives them,” he says. “I think what you’re really seeing here is a sort of misinterpretation of the question.”

Butler says that counter to the survey data, he finds borrowers are actually negotiating more than ever, though many end up re-signing with their existing lender once they agree to match a more competitive rate found elsewhere.

When it comes to finding a better deal, Butler, Smith and Jennings say it’s important to do your research, shop around and work with a broker who can help explore the available options.

“Shop around, shop online, shop at other banks,” Butler says. “There’s all kinds of online information about what rates are like — it’s so easy to look at mortgage rates today and compare terms and compare rates — so why not?”